Buying a house is a major milestone, but what happens when you have second thoughts or you can’t fulfill the agreement you signed? Backing out of a home purchase isn’t a decision made lightly, yet it’s a scenario that buyers might face. But what’s the real meaning of backing out of a home purchase?

In this guide, we’ll walk through what it means to step away from a real estate deal, the common situations that lead buyers to reconsider, and when backing out is still an option. We’ll also cover the protections that may help you exit a contract with fewer risks and share practical tips for navigating the process as smoothly as possible.

A Top Agent Can Find the Right Deal For You

HomeLight can connect you with a top-performing, trusted agent who has the experience to find you the right house at the right price. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

What does it mean to back out of a home purchase?

In real estate, backing out means a buyer decides to walk away from a home purchase after their offer has been accepted but before the transaction officially closes.

This action is more formally known as rescinding or voiding a residential home purchase agreement. It’s a legal process where you, as the buyer, decide not to proceed with the purchase of the property. This decision can occur at various stages, including after an offer is made but before it’s accepted, after signing a purchase agreement, or even days before the closing.

When you back out of a home purchase, you’re essentially deciding not to move forward with buying the property. While that can sometimes be the right call, it’s important to know that it may come with financial, legal, and even emotional consequences for both you and the seller.

What happens next largely depends on your contract and when you choose to back out. In some situations, you could lose your earnest money deposit or face other penalties. But if your contract includes the right contingencies and you’re still within the allowed time frame, you may be able to walk away with little to no fallout.

What are common reasons a buyer backs out?

Buyers don’t always end up following through on a home purchase, even after an offer is accepted. Sometimes something unexpected comes up during the process that makes them rethink the deal. Other times, it’s simply a matter of the situation no longer feeling right.

Here are some common reasons why you might decide to back out of a home purchase:

- Your loan financing fell through: It’s not uncommon for a mortgage loan to be initially approved but later denied due to changes in your financial situation or lending policies.

- You lost your job or income: A big change in your job situation can affect your ability to get financing, which might make you rethink your homebuying plans.

- You become ineligible for financing: Various factors, like a drop in your credit score or a higher debt-to-income ratio, can suddenly make you ineligible for the mortgage you were counting on.

- Your home appraisal came in too low: If the appraisal comes in lower than the price you agreed on, it can mess with your financing and might make you reconsider moving forward.

- Your home inspection uncovered a major issue: Finding major issues during the inspection, like structural damage or system failures, can be enough to make a buyer walk away.

- You are unable to sell your current home: If you’re depending on selling your current home to buy the new one, any delays or hiccups can force you to back out.

- Your title search found issues: Unresolved liens or legal issues found during the title search can make a property less appealing or even stop the sale altogether.

According to HomeLight’s Top Agent Insights for Q3 2025 report, a survey of more than 800 top real estate agents across the country, here are the top reasons buyers canceled a signed purchase agreement in 2025:

- Home inspection uncovers major issues: 27%

- Buyer’s financing falls through: 21%

- Buyer gets cold feet: 20%

- Seller refuses repair requests or concessions: 12%

- Appraisal comes in below the sale price: 6%

When can I back out of buying a house?

After looking at the common reasons buyers walk away, it’s clear that a deal can change course for a lot of reasons. Once those issues show up, it’s normal to start wondering what options are still on the table. Knowing when you can back out of buying a house helps you understand where you actually stand in the process. In general, you can safely back out of a home purchase during these key stages:

- During the contingency period: Most home purchase contracts include contingencies for financing, inspection, appraisal, and title search. (More on these later.) If issues come up during these contingency periods that can’t be worked out, you can usually walk away without any penalties.

- Before signing the purchase agreement: You can back out anytime before you sign the purchase agreement. Until that contract is signed, you’re not legally locked into the deal.

- When there’s a breach of contract by the seller: If the seller doesn’t meet certain parts of the contract, like failing to disclose defects or missing agreed timelines, you may have a valid reason to back out of the deal.

- During the attorney review period: In some states, there’s an attorney review period right after the contract is signed where either side can cancel the deal for almost any reason. This usually lasts about five days.

As with any legally binding contract, it’s important to know the exact terms and timelines in your purchase agreement. If you’re thinking about backing out, HomeLight recommends consulting a real estate attorney who can guide you based on your situation and local laws.

What happens when I back out of a home purchase?

Walking away from a home purchase isn’t always without consequences, and the impact can vary quite a bit. Depending on the situation, you could lose earnest money or trigger other contractual outcomes. That’s why it helps to understand what happens when I back out of a home purchase before making the call. Here are some common consequences of voiding the agreement:

- You could lose your earnest money deposit: If you back out of the deal without a valid contingency, the seller might be entitled to keep your earnest money deposit as compensation for the breach of contract.

- You could end up back at square one: Searching for a home, making an offer, and moving through early steps can take a lot of time and energy. If you back out, you’ll likely have to start the whole process again from scratch.

- Your mortgage preapproval could run out: Mortgage preapprovals have an expiration date. If you take too long to find another home, you may need to reapply, potentially facing different terms or rates.

- You could face legal action from the seller: Depending on how it affects the seller and what’s in your contract, backing out could sue you as they try to recover their losses.

- You could feel discouragement or relief: Emotionally, backing out can be a double-edged sword. While it can lead to feelings of discouragement or stress, it can also bring relief, especially if backing out is the best choice for your situation.

What contingencies protect a buyer when backing out?

When you’re considering backing out of a home purchase, certain contingencies in your contract can provide protection and legal grounds to do so without severe penalties. Here are some key contingencies that safeguard buyers:

- Financing contingency: Also known as a mortgage or loan contingency, this clause allows you to back out if you’re unable to secure a home loan. It’s a safeguard in case your loan approval falls through after signing the purchase agreement.

- Inspection contingency: The home inspection contingency lets you renegotiate or withdraw your offer based on the findings of a home inspection. It provides you with protection if major issues or repairs are discovered.

- Appraisal contingency: If the home appraises for less than the sale price, the appraisal contingency gives you the option to back out, as it can affect your loan-to-value ratio and mortgage approval.

- Title contingency: The title contingency protects you if there are issues with the property’s title, like unresolved liens or disputes over property boundaries.

- Home sale contingency: If you’re relying on the sale of your current home to finance the new purchase, the home sale contingency allows you to back out if you can’t sell your existing home within a specified time frame.

- Insurance contingency: Sometimes, getting homeowner’s insurance at a reasonable rate can be tough because of certain factors like location or property condition. An insurance contingency lets you back out if you can’t secure the coverage you need.

It’s important to go over your contingency options with your real estate agent and make sure they’re included in your contract when needed. An experienced agent can also help you figure out when it might make sense to waive or remove a contingency from your offer.

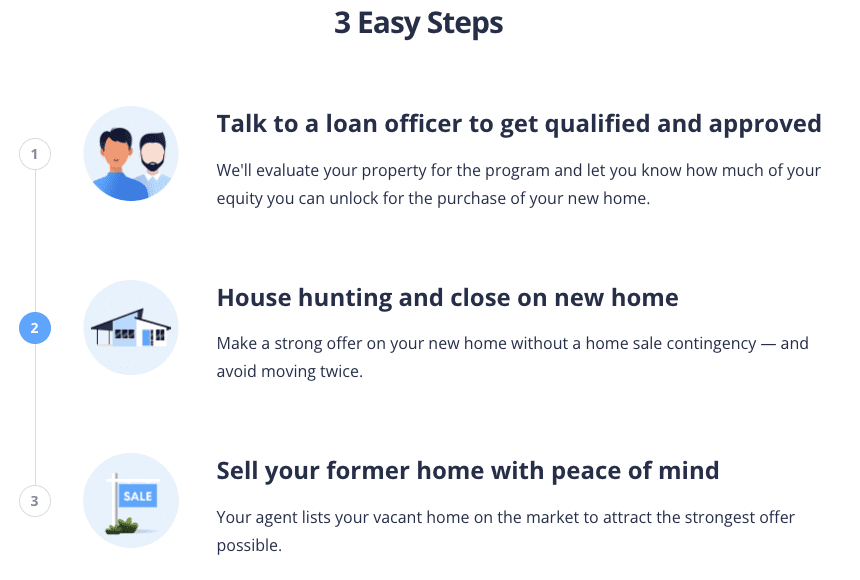

Can I make a non-contingent offer?

If you’re searching for a way to make a non-contingent offer or buy your next house before you sell your current home, contact us or ask your agent about HomeLight’s Buy Before You Sell program. This innovative program lets you unlock the equity in your current property to buy your next home, making your offer more attractive to sellers.

Here’s a short video illustrating how HomeLight Buy Before You Sell works:

When is it too late to back out of a home purchase?

Related to the points above about when you can back out of a home purchase, there are also moments where there’s basically no turning back, or at least where backing out gets a lot more complicated and costly. These include:

- After the contingency periods expire (you’ll likely forfeit your deposit)

- After signing the closing documents

- After you have taken possession of the home

You may also face financial penalties if you cancel the deal after your mortgage is finally approved and you’ve committed to the loan terms. Depending on your lender, withdrawing your purchase intent can lead to cancellation fees.

How to avoid trouble when backing out of a home purchase

Backing out of a home purchase can get tricky and sometimes expensive. But with the right know-how, you can lower the risks and avoid unnecessary headaches. Here are some tips to help you handle the process more smoothly:

- Understand your home purchase contract before signing: Be sure to review all the terms and conditions and know what you’re committing to so you don’t run into surprises later.

- Ask your lender about an earnest money guarantee: Some lenders offer programs to protect your earnest money deposit, providing an extra layer of security.

- Monitor contract timelines and deadlines: Staying on top of key dates helps you act in time and make decisions while you still have options.

- Include contingencies in your offer: Contingencies give you a legal way to back out of a purchase under certain conditions without facing penalties.

- Be proactive and plan: Thinking ahead about possible issues and having a backup plan can make it a lot easier to back out if you ever need to.

- Have a financial safety net: Make sure you’ve got enough cash set aside to cover unexpected costs, like the potential loss of your earnest money deposit or other fees that might come up.

- Communicate with the seller in writing: Check in with your agent about when and how to communicate with the seller and their agent. Many issues can be resolved more smoothly when you remain respectful and courteous.

- Know local laws: Real estate laws vary by state. Understanding these can help you better navigate the process and know your rights.

- Partner with a top real estate agent: A knowledgeable agent can guide you through the process, provide valuable advice, and advocate on your behalf.

We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs. It takes just two minutes to match you with the best real estate agents, who will contact you and guide you through the process.Find a top real estate agent near you

Before backing out of a real estate deal

Backing out of a home purchase isn’t uncommon, but it’s also not something to take lightly. Depending on your contract, timing, and the situation, the consequences can range from minimal to costly. That’s why understanding your contingencies and knowing your rights at each stage of the process is so important.

With the right preparation and awareness, you can make decisions that protect both your finances and your peace of mind. If you’re buying a home and want guidance along the way, use HomeLight’s Agent Match tool to team up with a proven agent who can protect your earnest money and find you the right home at the right price.

Frequently asked questions about backing out of a home purchase

A cooling-off period is a short window after signing a contract where you can still change your mind. It gives buyers or sellers a chance to step back without getting locked in right away. Not all real estate deals include one, and it depends on your state and contract terms. When it does apply, it can make backing out a lot less stressful.

Rescinding a contract usually means canceling it as if it never went into full effect. Terminating a contract means ending it after it’s already active and recognized. In real estate, both get you out of a deal, but the timing and reason behind each one can differ. The exact impact depends on what’s written in your agreement.

To renege on a contract means to go back on a promise or agreement after you’ve already committed. In real estate, it refers to backing out without a valid reason under the contract terms, basically breaking the deal after agreeing to it. This can sometimes lead to penalties or legal issues depending on the situation.

Yes, a seller can sometimes back out of an accepted offer, but it’s not always simple or risk-free. It usually depends on the contract terms and whether contingencies still apply. In some cases, they may face legal or financial consequences if they try to walk away without a valid reason. Once both sides are under contract, backing out gets a lot more complicated.

Header Image Source: (Brendan Stephens/ Unsplash)

English (US) ·

English (US) ·